- 22/12/2025

- Posted by: Thamizharasu Gopalsamy

- Category: business strategy

Every business faces risks, from market fluctuations and operational disruptions to cybersecurity threats and regulatory changes. Understanding how to manage risk in business isn’t just about avoiding problems—it’s about positioning your company to thrive even when challenges arise. Learning how to manage risk in business effectively can mean the difference between surviving disruption and being overwhelmed by it. This comprehensive guide will walk you through proven strategies to identify, assess, and mitigate business risks effectively.

What Is Business Risk Management?

Business risk management is the process of identifying, analyzing, and responding to potential threats that could negatively impact your organization’s capital, earnings, or operations. Rather than eliminating all risks (which is impossible), effective risk management helps you make informed decisions about which risks to accept, avoid, transfer, or mitigate.

The stakes are high. According to research, companies with mature risk management practices are 2.5 times more likely to outperform their peers financially. Yet many businesses still operate reactively, addressing risks only after they’ve materialized into costly problems.

Why Risk Management Matters More Than Ever

Today’s business environment is increasingly complex and interconnected. Digital transformation, global supply chains, climate change, and geopolitical instability have multiplied the types and severity of risks organizations face. A single cybersecurity breach can cost millions in remediation and reputational damage. Supply chain disruptions can halt production for weeks. Regulatory non-compliance can result in devastating fines.

Effective risk management provides several critical benefits:

- Financial protection: Prevents costly losses from materializing risks

- Competitive advantage: Enables you to pursue opportunities competitors find too risky

- Stakeholder confidence: Builds trust with investors, customers, and partners

- Operational resilience: Ensures business continuity during disruptions

- Strategic clarity: Improves decision-making by quantifying uncertainties

Step 1: Identify All Potential Risks

You can’t manage risks you don’t know exist. The first step in how to manage risk in business is creating a comprehensive inventory of potential threats across all areas of your operation. This foundational step in how to manage risk in business requires systematic analysis across all departments and functions.

Categories of Business Risk

Strategic Risks: These threaten your business model, competitive position, or long-term objectives. Examples include new competitors entering your market, technological disruption making your products obsolete, or major shifts in customer preferences.

Operational Risks: Day-to-day business operations involve numerous risks, from equipment failures and supply chain interruptions to quality control issues and employee safety hazards.

Financial Risks: Market volatility, currency fluctuations, credit risk, liquidity issues, and rising interest rates can all impact your financial stability.

Compliance and Legal Risks: Failure to comply with regulations, contract breaches, intellectual property disputes, and employment law violations can result in significant penalties.

Reputational Risks: In the age of social media, negative publicity, customer complaints, data breaches, or ethical scandals can quickly damage your brand.

Technology Risks: Cybersecurity threats, system failures, data loss, and IT infrastructure vulnerabilities pose increasing dangers to modern businesses.

Risk Identification Methods

Use multiple approaches to uncover risks across your organization:

Brainstorming sessions: Gather teams from different departments to identify risks from their unique perspectives. Finance sees different threats than operations or marketing.

SWOT analysis: Examining your weaknesses and threats naturally surfaces potential risks that might impact your business.

Historical data review: Analyze past incidents, near-misses, and losses to identify patterns and recurring vulnerabilities.

Industry benchmarking: Study what risks have impacted competitors and similar businesses in your sector.

Expert consultation: Bring in specialists for technical areas like cybersecurity, legal compliance, or financial risk.

Process mapping: Document key business processes and identify points where failures could occur.

Step 2: Assess and Prioritize Risks

Not all risks deserve equal attention. After identifying potential threats, you need to evaluate their likelihood and potential impact to prioritize your response efforts.

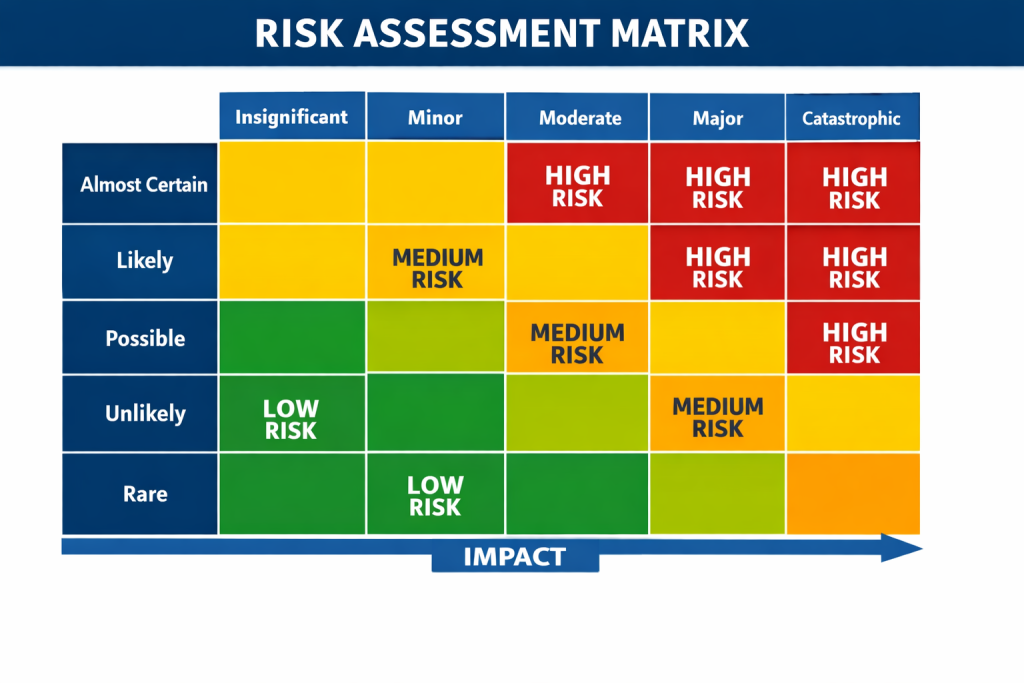

The Risk Assessment Matrix

A simple but effective tool is the risk matrix, which plots each risk on two dimensions:

Likelihood: How probable is this risk to occur? (Rare, unlikely, possible, likely, almost certain)

Impact: If it occurs, how severe would the consequences be? (Insignificant, minor, moderate, major, catastrophic)

Risks that are both highly likely and highly impactful demand immediate attention. Those that are unlikely and low-impact may simply be accepted and monitored.

Quantifying Risk

For significant risks, try to estimate potential financial impact in concrete terms. A cybersecurity breach might cost $500,000 in remediation plus $2 million in lost business. A key supplier failure might halt production, costing $50,000 per day. These numbers help justify investments in risk mitigation and make trade-offs clearer.

Don’t forget to consider cascading effects. A single risk event can trigger multiple consequences. A data breach causes immediate costs but also damages reputation, triggers regulatory investigations, and may result in lawsuits.

Risk Velocity

Some risks develop slowly, giving you time to respond. Others strike suddenly. Consider the “risk velocity” when prioritizing. A gradual market shift might be lower priority than a sudden cyber threat, even if both have similar potential impacts.

Step 3: Develop Risk Response Strategies

Once you’ve prioritized risks, determine the most appropriate response for each. You have four basic strategies:

Risk Avoidance

Sometimes the best response is to eliminate the risk entirely by not engaging in the risky activity. If expanding into a politically unstable region poses unacceptable risks, don’t expand there. If a particular supplier has reliability issues that can’t be resolved, find a different supplier.

Avoidance makes sense when risks are severe and mitigation is prohibitively expensive or ineffective. However, avoiding all risks means avoiding opportunities, so use this strategy selectively.

Risk Reduction (Mitigation)

Most risks can be reduced to acceptable levels through preventive or detective controls. This is typically the most common and cost-effective approach when learning how to manage risk in business.

Preventive controls stop risks from occurring: employee training, quality assurance processes, cybersecurity measures, equipment maintenance, and safety protocols.

Detective controls identify issues quickly so you can respond before they escalate: monitoring systems, audits, performance reviews, and customer feedback mechanisms.

For example, to reduce cybersecurity risk, you might implement multi-factor authentication, conduct regular security training, maintain updated firewalls, and perform penetration testing.

Risk Transfer

Transfer risk to another party, typically through insurance or contractual agreements. Property insurance transfers fire risk to the insurer. Liability insurance covers lawsuit costs. Outsourcing certain functions transfers operational risk to the vendor.

Risk transfer doesn’t eliminate the risk—if your outsourced vendor fails, you still have a problem—but it shifts financial burden and sometimes management responsibility. Always ensure you’re transferring to capable, reliable parties and that contracts clearly define responsibilities.

Risk Acceptance

Some risks are too unlikely or too minor to justify mitigation costs, or the cost of avoidance would exceed potential losses. In these cases, consciously accept the risk and prepare to manage consequences if they occur.

Document accepted risks explicitly so stakeholders understand the decision was deliberate, not an oversight. Set tolerance thresholds and review accepted risks periodically as conditions change.

Step 4: Implement Risk Controls

Strategy without execution is meaningless. Once you’ve decided how to respond to each priority risk, implement specific controls and safeguards.

Creating an Action Plan

For each significant risk, develop a detailed action plan that includes:

- Specific control measures to implement

- Responsible individuals or teams

- Implementation timeline

- Required budget and resources

- Success metrics to measure effectiveness

Assign clear ownership. Someone must be accountable for implementing and maintaining each control, or it simply won’t happen amid competing priorities.

Key Risk Controls by Category

For operational risks: Implement standard operating procedures, cross-train employees to reduce key person dependency, diversify suppliers, maintain adequate inventory buffers, and establish backup facilities or equipment.

For financial risks: Maintain adequate cash reserves, diversify revenue streams, use hedging strategies for currency exposure, establish credit policies, and implement rigorous budgeting and forecasting processes.

For compliance risks: Create a compliance calendar tracking all regulatory deadlines, conduct regular compliance audits, implement document management systems, provide ongoing compliance training, and establish clear reporting channels for concerns.

For cybersecurity risks: Deploy layered security (firewall, antivirus, intrusion detection), enforce strong password policies and multi-factor authentication, conduct regular security awareness training, maintain current software patches, encrypt sensitive data, and implement access controls based on role requirements.

For reputational risks: Monitor social media and online reviews, establish crisis communication protocols, train spokespeople, build relationships with key media contacts, deliver consistent quality, and address complaints promptly and professionally.

Step 5: Create Business Continuity and Disaster Recovery Plans

Even with excellent preventive controls, some disruptions will occur. Business continuity planning ensures you can maintain or quickly resume critical operations after a significant incident.

Business Impact Analysis

Start by identifying your critical business functions and the maximum tolerable downtime for each. Can your business survive 24 hours without your website? One week without access to customer data? Understanding these tolerances guides your continuity planning priorities.

Recovery Strategies

Develop specific procedures for recovering from different scenarios:

Data backup and recovery: Maintain regular backups stored in multiple locations, including off-site or cloud storage. Test restoration procedures regularly—untested backups are worthless.

Alternative work arrangements: Establish remote work capabilities, identify backup facilities, and create plans for relocating operations if your primary location becomes unavailable.

Supply chain alternatives: Maintain relationships with backup suppliers and document alternative sources for critical inputs.

Communication plans: Predetermine how you’ll communicate with employees, customers, suppliers, and other stakeholders during a crisis. Include contact lists, communication channels, and key messages.

Crisis management team: Designate a team responsible for activating and coordinating the continuity plan, with clear roles and decision-making authority.

Testing and Exercises

Plans that sit on shelves are plans that fail when needed. Conduct regular exercises ranging from tabletop discussions to full-scale simulations. These exercises reveal gaps, familiarize teams with procedures, and build muscle memory for crisis response.

Step 6: Monitor, Review, and Update

Risk management isn’t a one-time project—it’s an ongoing process. The business environment constantly evolves, introducing new risks and changing the profile of existing ones.

Continuous Monitoring

Implement systems to track key risk indicators (KRIs) that provide early warning of emerging threats. For example:

- Financial KRIs: Days sales outstanding, debt-to-equity ratio, cash flow metrics

- Operational KRIs: Equipment downtime, defect rates, employee turnover

- Cybersecurity KRIs: Failed login attempts, unusual network traffic, unpatched systems

- Compliance KRIs: Overdue licenses, unresolved audit findings, training completion rates

Set thresholds that trigger alerts when metrics move into concerning territory, allowing proactive intervention before issues escalate.

Regular Risk Reviews

Schedule periodic risk assessments (quarterly or annually, depending on your industry’s pace of change) to:

- Identify new risks that have emerged

- Reassess the likelihood and impact of existing risks

- Evaluate the effectiveness of current controls

- Update response strategies as needed

- Remove risks that are no longer relevant

These reviews should involve stakeholders from across the organization, as different departments encounter different risks and offer valuable perspectives.

Learning from Incidents

When risk events occur, conduct thorough post-incident reviews to understand what happened, why controls failed, and how to prevent recurrence. Share lessons across the organization so others can learn from the experience.

Building a Risk-Aware Culture

Technical risk management processes are necessary but insufficient. Understanding how to manage risk in business goes beyond processes and tools—the most resilient organizations cultivate a culture where risk awareness is embedded in everyday decision-making.

Leadership Sets the Tone

Risk culture starts at the top. When leaders openly discuss risks, admit uncertainties, and value careful analysis over blind optimism, it gives permission for others to do the same. Conversely, when leaders shoot the messenger or punish those who raise concerns, risk information stops flowing upward.

Model the behavior you want to see. Ask “what could go wrong?” in planning meetings. Celebrate employees who identify risks before they materialize. Make risk considerations a standard part of project approvals and strategic decisions.

Empower Employees

Front-line employees often spot risks first but may hesitate to report them. Create clear, safe channels for reporting concerns without fear of retribution. Respond promptly and transparently to reports, even when issues can’t be immediately resolved.

Provide risk management training so employees understand both the organization’s risk framework and their role within it. When people understand why controls exist, they’re more likely to follow them.

Balance Risk and Opportunity

A healthy risk culture doesn’t mean avoiding all risks—it means taking calculated risks with eyes open. Encourage innovation and entrepreneurship while requiring thoughtful analysis of potential downsides and mitigation strategies.

Common Risk Management Mistakes to Avoid

Even experienced businesses make critical errors in how they manage risk:

Focusing only on insurable risks: Insurance is important, but many significant risks (reputational damage, strategic missteps, market disruption) can’t be insured away.

Neglecting emerging risks: Organizations often focus on familiar, historical risks while missing new threats. Make time to consider “what’s different now?” and “what might we be missing?”

Treating risk management as a compliance exercise: Checking boxes satisfies auditors but doesn’t protect your business. Focus on substance over paperwork.

Siloed risk management: When departments manage risks independently without coordination, interdependencies and cascading effects go unrecognized. Enterprise risk management provides an integrated view.

Analysis paralysis: Perfect risk assessment is impossible. Make reasonable judgments based on available information and move forward rather than endlessly analyzing.

Overconfidence in controls: No control is perfect. Maintain healthy skepticism and backup plans even for well-controlled risks.

Technology and Tools for Risk Management

Modern software solutions can significantly enhance risk management capabilities:

Risk management platforms: Integrated systems like LogicManager, Resolver, or RiskWatch help document risks, track controls, manage incidents, and generate reports from a central repository.

Data analytics and AI: Advanced analytics can identify patterns in large datasets that humans miss, predicting potential risks based on historical trends and external factors.

Cybersecurity tools: Specialized security information and event management (SIEM) systems, vulnerability scanners, and threat intelligence platforms help protect against digital threats.

Scenario planning software: Tools that help model different scenarios and their potential impacts on your business support better strategic risk decisions.

Compliance management systems: Automated tracking of regulatory requirements, deadlines, and documentation ensures nothing falls through the cracks.

While technology is valuable, remember it’s a tool, not a solution. The most sophisticated software is worthless without good processes, skilled people, and organizational commitment.

Measuring Risk Management Success

How do you know if your risk management efforts are working? Track these indicators:

Leading indicators: Number of risks identified and assessed, percentage of employees completing risk training, control implementation rates, audit findings resolved.

Lagging indicators: Actual losses from risk events, insurance claims, regulatory violations, customer complaints, unplanned downtime.

Maturity assessments: Periodic evaluations of your risk management program’s sophistication using frameworks like the Risk Management Maturity Model.

The ultimate measure of success is resilience—the ability to withstand shocks and continue operating effectively. While this is hard to quantify until tested, organizations with strong risk management consistently demonstrate better crisis performance than unprepared competitors.

Conclusion: Making Risk Management Part of Your Business DNA

Learning how to manage risk in business is one of the most valuable investments you can make. It protects your hard-earned assets, preserves stakeholder trust, and enables you to pursue opportunities competitors might fear. Mastering how to manage risk in business requires commitment, but the payoff in resilience and competitive advantage is substantial.

Start where you are. You don’t need a perfect, comprehensive risk management system on day one. Begin with identifying your most critical risks, implementing basic controls, and building from there. Small businesses can manage risk effectively with straightforward approaches—sophisticated frameworks come as you grow.

The key is making risk management continuous and integrated rather than episodic and separate. When risk considerations become a natural part of planning, decision-making, and operations, you’ve built genuine resilience.

Remember that managing risk doesn’t mean eliminating uncertainty or avoiding all potential problems. It means understanding what could go wrong, preparing appropriately, and having the agility to respond when the unexpected occurs. In an increasingly volatile business environment, that capability may be your most important competitive advantage.

Take action today. Gather your team, identify your top five risks, and start developing response strategies. Your future self will thank you when you successfully navigate the challenges that derail less-prepared competitors.

Leave a Reply

You must be logged in to post a comment.